A Cease-and-Desist Letter to the Management of Teekay Tankers

We have heard enough. We must all stand firmly together and demand management not announce a large "fleet renewal" plan. If they cannot, we must insist on a sale or liquidation of the business.

Get the bake-off under-way. Call Evercore, call Jefferies. Let’s get the process going. We have seen enough. I, for one, cannot bear to watch any longer. It is like a car crash in slow motion with your favorite driver at the wheel. Teekay Tanker management is top notch, the only criticism to-date is that perhaps they have been too conservative.

But let us tell you what is going to happen. The writing is on the wall. It is not a secret; people are talking openly about it.

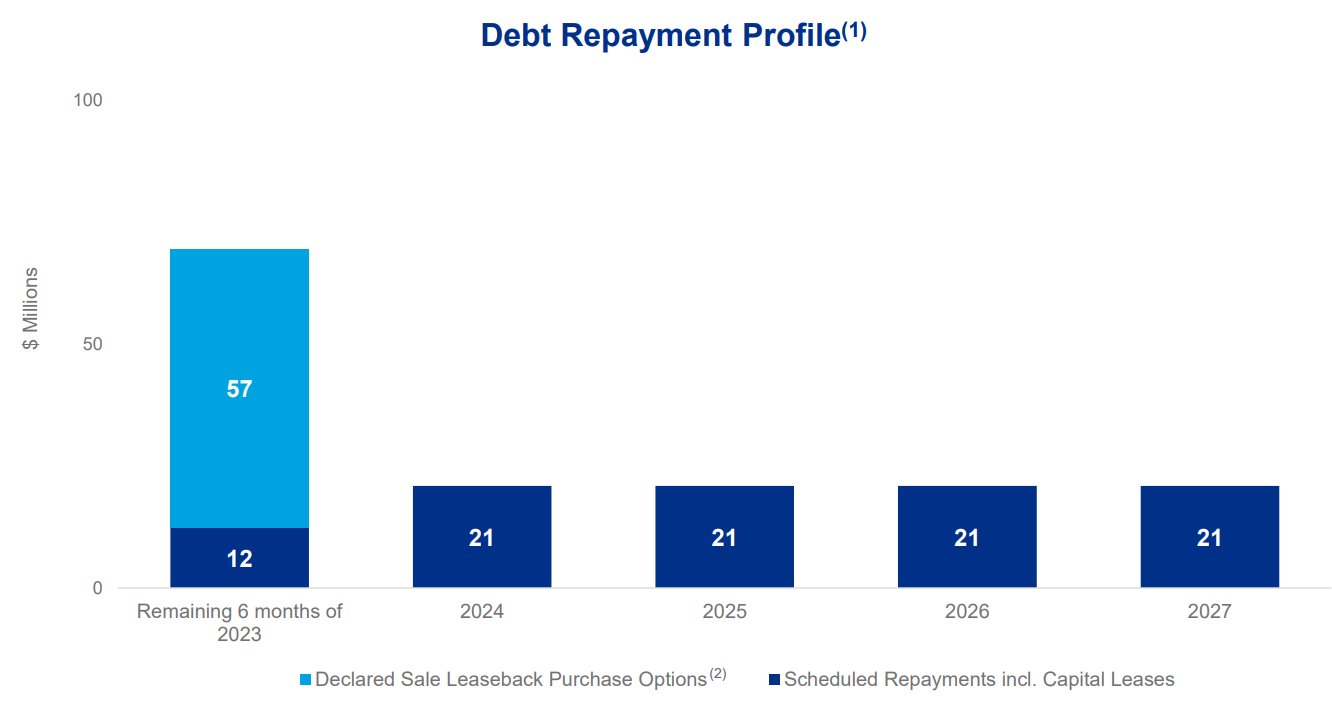

Given the continued strength in the tanker market in the first part of the third quarter, we are now net debt free, further supporting our ability to reinvest in the TNK fleet when the time is right and to return capital to our shareholders.

And our view for the long-term value creation for shareholders is that we need to reinvest and we're going to do that in a disciplined way when the opportunities arise.

Our number one priority is to build capacity for making reinvestments in the fleet at the right time when the opportunities arise. And that is one of the things that we're focused on. We haven't acquired a tanker since 2017.

CFO Stewart Andrade, 2Q Earnings Call

They are going to do it. They are GOING TO DO IT.

Do what?

They are going to blow all their damn money on some bloody newbuild program or modern acquisitions. They haven’t bought a ship since 2017, they have the itch! Well they also hadn’t paid a dividend, I don’t believe, since 2018 up until May of this year. But we digress.

“To create long-term value for the next 20 years” they will say. “To keep with the long Teekay legacy of good stewardship of capital and the environment, we have decided to order the most EEXI / alternative-fuel compliant engines to meet the IMO 2030 and beyond targets”, I can hear it now.

But there is still time to stop it!

Gentlemen, you have done well. You have taken us this far. TNK has been the best performing equity across the tanker universe the last 5 years, up ~468% or something. Amazing! Now please slowly back-away from your work stations.

Do not make any drastic movements. Do not place any distressed calls to China or South Korea, or even Japan.

We can talk through this if you are open. It is OK to be the management team of the older tanker fleet. It is 2023, age is just a number. I know Tor Olav is running around ordering VLCCs left and right, getting press, riding the beginning of the cycle, we heard the story.

But you have a cash flow machine. You have the best performing stock. Tor Olav would love to have what you have. Cherish it.

And look! You guys are in the news too.

The only problem is none of these articles talk about how Teekay Tankers can become a dividend / shareholder return machine. How you can trade at a premium because investors will flock to the high yield and strong governance.

While there were only 2.5 analysts on the call, legendary shipping analyst Jonathan Chappell just wanted you to say you could pay some more dividends. We need all the analysts we have left! We can’t afford to lose any more. Please give Jon what he wants.

And being net debt free today, do you anticipate just kind of saving up capital for that 1Q event where you can really clear the decks on the sale and leaseback, or if there is a seasonal uplift, let's say, starting in the fourth quarter, does that make that not really mutually exclusive with ratcheting up either a special dividend or maybe the base dividend?

For starters, the Company does not need to be in a net cash position, you can have a little debt. So it will be OK to take on some debt in finalizing these purchase options.

But alas, here you are, with no leverage and your upcoming purchase options. What a ride it has been. Low break-evens to weather any storm, finally ready to rebuild after years of managing the ship through some narrow channels. Now you can relax, place some newbuild orders, smash some champagne on the bow, celebrate the future.

But now is not the time for that, now is the time to harvest and reward. I know, it is not as exciting, or what you want to hear.

This is what we propose. We hope that you can agree.

Declare that you will not acquire any vessel or place a newbuild order until 1) TNK trades above NAV or 2) a minimum of 2.0 years passes or 3) 30% special dividend is paid

Create a formal dividend policy similar to Star Bulk. TNK to pay-out all cash above a ~$1.75M/vessel cash balance; this can be revisited should leverage reach 40%. Bonus points if you add it to the website

Do not target additional de-levering (even if you could). Company should seek ~20% leverage

Appoint a “Shareholder Representative” to the Board - this individual to represent the shareholders focused on return of capital

Other items we would like to discuss:

What is going on with Teekay Corporation?

While I think we need to figure out how to divert from the impending doom of ordering vessels, our view is that Teekay Corporate should consider stepping down from the Board.

I know this sounds a little silly given the ownership structure, but hear us out. And we don’t mind if they keep their shares, but don’t they seem distracted? They are currently custodians of a handful of bank accounts and treasuries. $136M to be exact.

They sold LNG - the most future focused shipping sector - before the biggest earnings spike in history.

And I imagine they are looking for new investments in ‘energy transition’. They have a small buy-back program of their own shares. Maybe you can do an Eagle and buy them out at a 30% premium? Or do a Dorian and tender shares half way to NAV?

This is a long way of saying we don’t have much comfort that they want to maximize the value of TNK today. The two tiered voting system is poor corporate governance and they have no vision or path - they have abandoned their mandate for control.

So who could help extract value in TNK and close the 35% discount to NAV?

The top name that comes to mind is Uncle John and the team at Frontline. They have been active in other peer names and trade at a premium to NAV. Perhaps the Fredriksen premium could unleash that 35% in TNK?

INSW could be interesting, although this would create more of a mixed fleet. They have the newbuild VLCCs which are dual fueled and the Company would be well positioned to manage end of life legacy vessels, which will have more importance in the years to come.

And then there is Euronav. I am not sure you would want to get involved in that situation, but they have newbuilds to scratch that itch, and they need a CEO!

In summary, we hope that you will pull back from the cliff of shareholder destruction. There are a handful of paths to super charge the TNK equity given your immense cash flow potential and future yields. These items must be explored at all cost before repeating history and renewing the fleet at this time.

Thank you,

Three Sheets

P.S to readers and shareholders - If all else fails, Teekay lists the below emergency hotline for questionable internal control and fraud. A large fleet renewal at this point in the cycle may just qualify.